Imagine earning a steady income, yet every month you find yourself struggling to invest and grow your wealth — what if you could change that? You want to save, invest, and plan for the future, but somehow only a small portion of your earnings ever makes it to an investment account.

This is what Mumbai-based Rohit Chauhan, a chartered accountant, began noticing as a common problem while working in the corporate sector. “If people have the capacity to invest ₹100, they end up investing only ₹80,” he observed. It wasn’t a matter of intent but of habit—financial discipline often gave way to impulse spending, and the need for a buffer held back potential investments.

This gap sparked the foundation of what would eventually become Ingood, a Mumbai-based fintech startup.

Rohit teamed up with Anuradha Singh, a fellow chartered accountant with sharp operational expertise. Together, they designed a platform that would do more than just track expenses—it would automatically invest surplus funds.

Their bold move was integrating credit card management with investment tools, allowing users to leverage the 40-day interest-free period on credit cards to invest smarter without affecting liquidity.

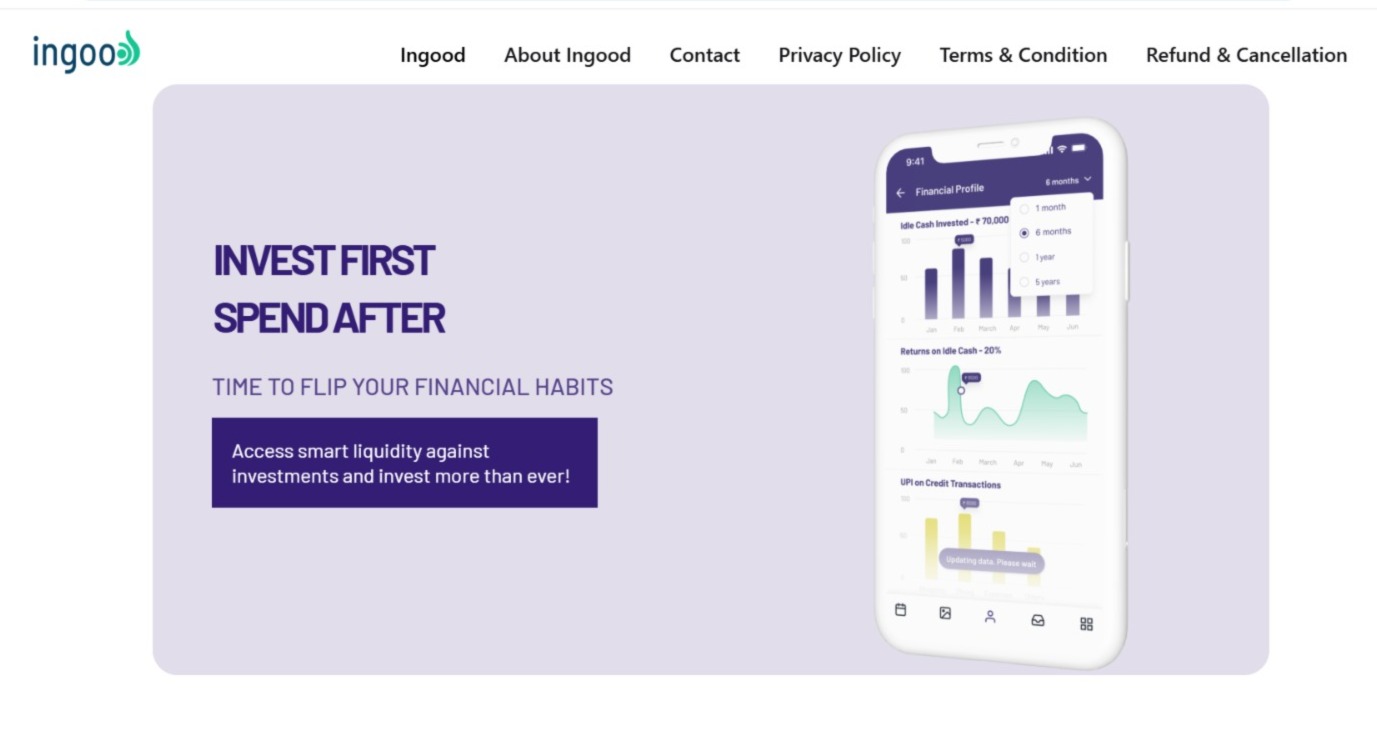

Redefining Financial Discipline: Ingood’s Services and Offerings

Built by Rohit Chauhan, Anuradha Singh, the Ingood app, developed by this Mumbai-based fintech startup, is designed to simplify financial management while encouraging smarter habits. It’s more than just an investment tool—it’s a personal finance companion.

Spending Analysis: The app tracks credit card usage to calculate an individual’s average monthly spending. Whenever the current month’s expenses fall below that average, the difference—your surplus—is identified as potential savings.

Automated Investments: Users choose what portion of that surplus they want to invest. At the end of the month, Ingood automatically moves that amount into selected instruments, either index funds with 10%+ potential returns for risk-takers or instant redemption funds offering 6–7% returns with full liquidity.

“The money is readily available to you,” explains Chauhan, emphasizing that flexibility is never compromised.

Credit Card Integration: Ingood links users’ existing credit cards and leverages the 40-day interest-free credit window. “For one month, we have already earned a return on that money which you have invested at the start,” Chauhan explains, showcasing how the platform turns surplus money on your credit card into compounding returns.

Spending Insights: The app also offers detailed spending reports, helping users develop financial awareness. Chauhan shares a revealing anecdote: “One user spent ₹33,000 on Zomato in 3 months, and his salary was just ₹35,000 a month.” These insights often become a wake-up call, nudging users toward better money management.

Introducing Smart Sweep by Ingood:

Say hello to a smarter way to manage your money. With Ingood’s innovative Smart Sweep feature, your idle funds are automatically optimized—seamlessly integrating investments and credit management. It’s not just better than traditional savings—it’s the future of financial intelligence.

Where and How Ingood Plans to Scale

Currently in its pre-launch phase, the Ingood app is being tested by a select group of developers, friends, and family. “We’ve released it to a closed group, and we’ll open it up to a larger set in the next 10 days or so,” shares Rohit Chauhan, hinting at a full-fledged rollout on the Google Play Store.

The platform’s initial focus is on Tier 1 and Tier 2 cities, specifically targeting IT professionals and young earners who are eager to take control of their finances. Whether someone earns ₹40,000 or upwards of ₹3 lakhs, the app is designed to serve a wide income bracket with equal efficiency.

Backed by Afthonia Labs, their growth approach is deliberately organic, relying on word of mouth, early adopters, and user trust rather than aggressive marketing.

The goal is to acquire 20,000- 30,000 users in the first six months and gather deep insights into spending behavior. “At this stage, revenue isn’t our priority. Understanding our users is,” Chauhan emphasizes during the interview with Empowering Indians.

Challenges, Setbacks, and the Road to Launch

Building Ingood wasn’t a linear journey—it was a leap of faith carved out of conviction. In December 2022, Rohit Chauhan, the Mumbai-based founder, made a bold decision: he quit a cushy job paying ₹26–27 lakhs a year to chase his entrepreneurial dream. In hindsight, he calls it “a bad call”—not because he didn’t believe in the idea, but because he underestimated the climb.

“You can’t raise funds at the idea stage; you need to show up with a site,” Chauhan candidly shares. His original plan involved launching a co-branded credit card, but this proved nearly impossible without venture capital support. “Issuing your own co-branded credit card is like a mammoth of a job,” he admits, as banks and NPCI remained inaccessible for early-stage founders.

Amid these roadblocks, instead of issuing their own card, they pivoted to mapping existing credit cards—a workaround that dramatically accelerated Ingood’s development. This strategic shift not only made the product more agile but also kept it user-centric.

The journey wasn’t cheap. With ₹20–27 lakhs invested from their own pockets, Chauhan and Singh bootstrapped the entire development. Collaborating with tech partners like Cybrilla, SETU and ZET, they built a product from scratch. “We’ve been building this for the last seven months,” Chauhan says proudly. The first working delivery came just 15 days before the interview—a significant milestone that marked months of tireless work.

From One-Room Homes to High Finance: The Making of a Resilient Founder

Rohit Chauhan’s journey began in Patna, Bihar, where his family lived in a single-room home. Financial hardship interrupted his education in the 7th grade, but his sister—a chartered accountant herself—brought him to Mumbai and mentored him through his CA journey.

Rohit supported himself on an internship stipend that started at just ₹3,500. Yet, determination pushed him forward. He cracked his CA entrance exam with an impressive score of 185/200, setting the stage for a high-flying career.

From an initial role at J.P. Morgan to working in alternative investment funds, he rose through the ranks, earning ₹26–27 lakhs annually by 2022.

However, he left the well-paying job to embark on his entrepreneurial journey.

Meanwhile, Anuradha Singh’s experience spans asset reconstruction, credit operations, and financial restructuring. Her clarity in execution and problem-solving mindset played a key role in turning InGood into a product rather than just an idea.

Together, they embody complementary strengths: vision, grit, and operational precision.

Vision and Plan Ahead

Chauhan and Singh have an ambitious vision for Ingood. They aim to empower India’s 50–60 crore underserved earners (those making ₹10,000–30,000 monthly), who lack access to investment opportunities and credit cards. “I want to capitalize on the growing UPI and e-commerce penetration,” says Chauhan. His plan is to introduce mutual fund-backed credit cards to serve this demographic, offering an alternative to high-interest credit cards used for small purchases like mobile phones.

“We want to sell investment, not credit cards,” he asserts at the end of the Empowering Indians interview.